Why Equinor might be the best energy stock for natural gas exposure:

At Muffett investments, we are constantly looking for ways to escape financial repression. We do not have a positive outlook for the UK economy where we are based and so we look outside UK to park our investments. One such countries that interest us is Norway. There are two reasons for this. One is its relatively low Debt- GDP ratio of 55% which is better than most of the G7 nations. The other reason is their sovereign wealth fund which is the largest in the world at around $2 trillion dollars.

This is the monthly chart of GBPNOK. As you can see, inspite of favourable economic profile the Norwegian kroner has weakened against the British Pound. we are however happy that this is the case. We are looking to diversify from the pound and the Norwegian Kroner is one such currency that we are looking at.

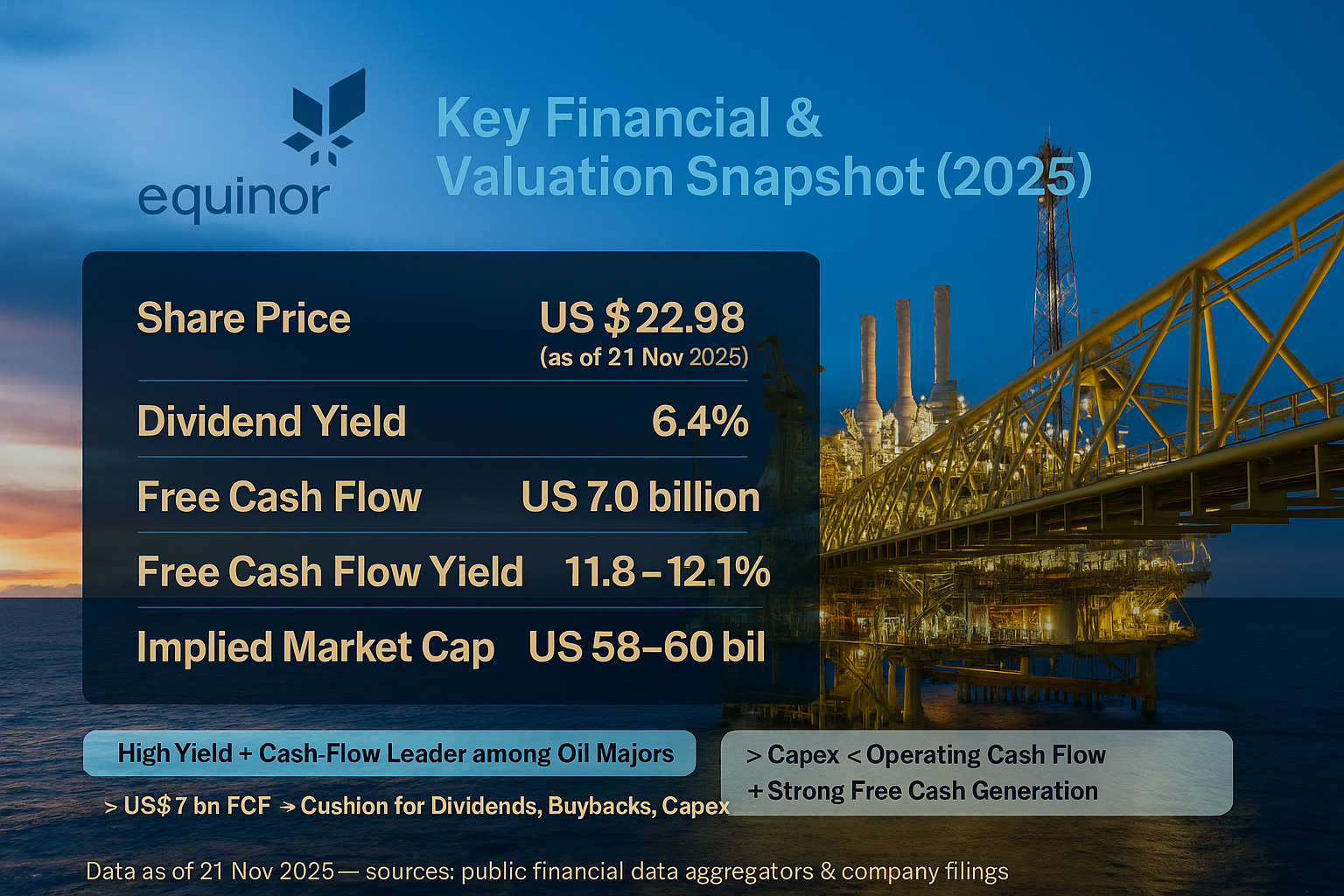

so combining our outlook on the Norwegian kroner and our interest in oil and particularly natural gas, we are pointing our focus on Equinor. If you see the infographic at the top, Equinor has a free cash flow yield of nearly 12% which is one of the highest among the Oil majors.

More about Equinor:

Equinor ASA is the Norwegian energy major formerly known as Statoil. The company produces ~2 million barrels of oil equivalent per day, with about two‑thirds of output coming from Norway’s continental shelf. . The company plans to increase total oil and gas production by more than 10 % between 2024 and 2027 and has lifted its 2030 production target to 2.2 million boe/d

Equinor's strategy is to optimize a world-class oil and gas portfolio to fund a competitive dividend and share buybacks, while prudently growing in renewables and low-carbon solutions. The numbers speak for themselves:

Free Cash Flow (FCF): The company projects a staggering $23 billion in cumulative FCF for 2025-2027. This is the lifeblood for everything else—funding new projects, paying down debt, and, most importantly for investors, rewarding shareholders.

Capital Distribution: In 2025 alone, Equinor plans to return $9 billion to shareholders. This consists of a steady quarterly cash dividend of 37 cents per share for the 4th quarter and a massive $5 billion share buyback program.

Resilient Balance Sheet: Their net debt ratio stood at a healthy 11.9% at the end of 2024. This financial fortitude provides a crucial buffer against market downturns.

Equinor’s assets:

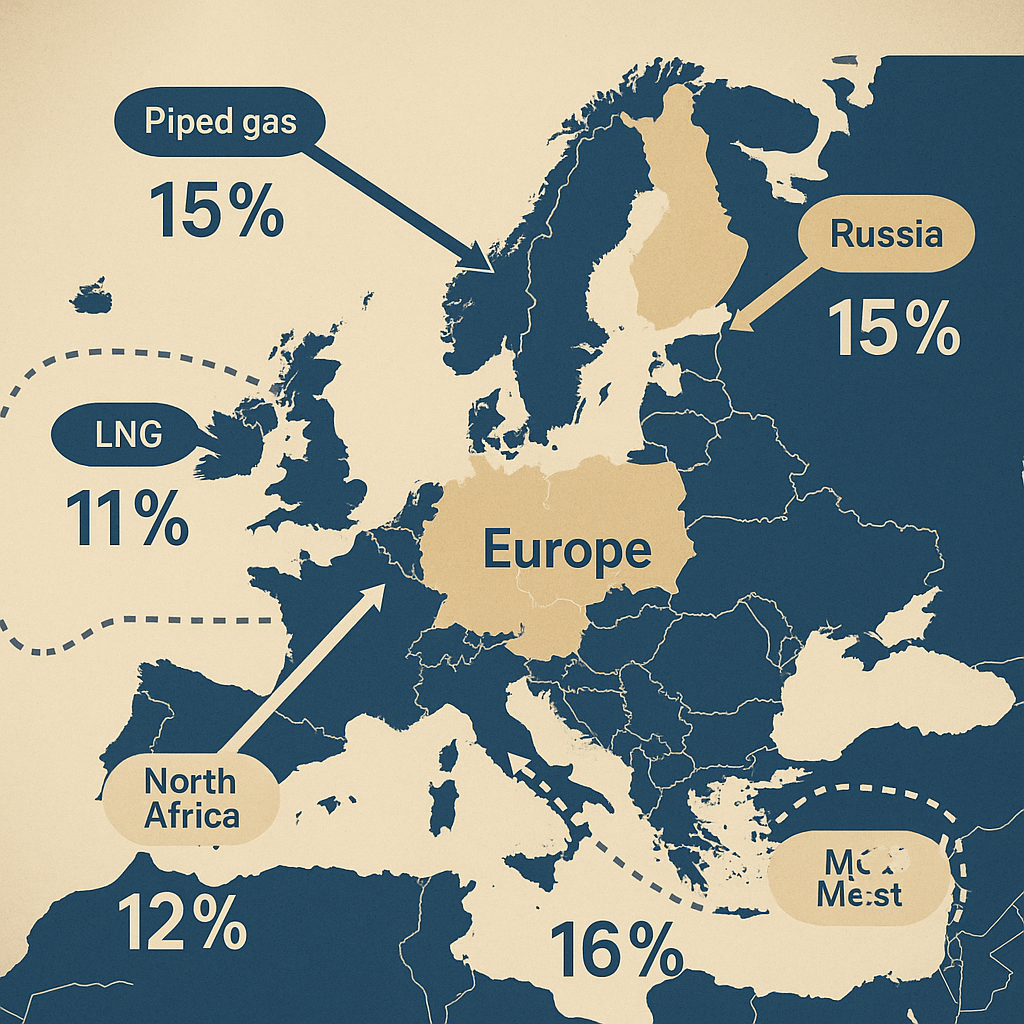

E&P Norway : The Norwegian Continental Shelf (NCS) is the foundation of Equinor's business. With giants like Johan Sverdrup and Johan Castberg oil production is predicted to increase over the next 3 years. Troll gas field is one of the largest offshore gas field ever discovered with proven resources of 1.3 trillion cubic metres. It accounts for 40% of the gas in the norwegian continental shelf and it produces 30% of the gas that is exported to Europe. Norway accounts for 11% of the European natural gas imports. It has favourable cost metrics with production costs of $2 and European gas prices of $13. This is a cashflow machine. If natural gas prices spike in the US, then LNG prices will rise and increase the European natural gas prices. This will automatically fill the coffers of Equinor. The NCS benefits from a favourable tax regime that provides resilience in low-price environments. A pipeline of 19 near-term projects ensures production remains around 1.25-1.4 million barrels of oil equivalent per day (boe/d) through 2035, guaranteeing long-term, low-cost cash flows.

E&P International (The Growth Engine): This segment is being transformed through strategic moves. The formation of a UK joint venture with Shell which will combine the UK assets of both companies will create the country's largest oil and gas producer, capturing significant synergies. Meanwhile, major project start-ups in Brazil (Bacalhau in 2025, Raia in 2028) and the US (Rosebank in 2027) are set to drive international production growth to over 950,000 boe/d by 2030.

Marketing, Midstream & Processing (MMP - The Profit Maximizer): This is where Equinor's trading prowess shines. The MMP segment consistently delivers strong earnings by leveraging its vast infrastructure and logistical capabilities to optimize the value of every molecule produced. It is a key differentiator that captures extra value from market volatility.

In our view, if Russian gas is phased out, then the most cost advantageous way to replace the gas is to get piped gas from Norway and piped gas from North Africa. Equinor already plans to increase the number of wells in Troll gas field to increase production. In our view, the gas from the middle east could be problem in the future if geopolitical conflict escalates. This will increase the gas prices in Europe and Equinor automatically benefits from this. This is our biggest interest in Equinor. It is strategically located to benefit from any kind of geopolitical disruption to energy supplies. The American natural gas companies will need LNG export terminals which will increase the cost.

On top of this, Equinor has exposure to Marcellus shale gas where it has a noncontrolling interest. But it will benefit from rising gas prices from data centre demand and LNG exports.

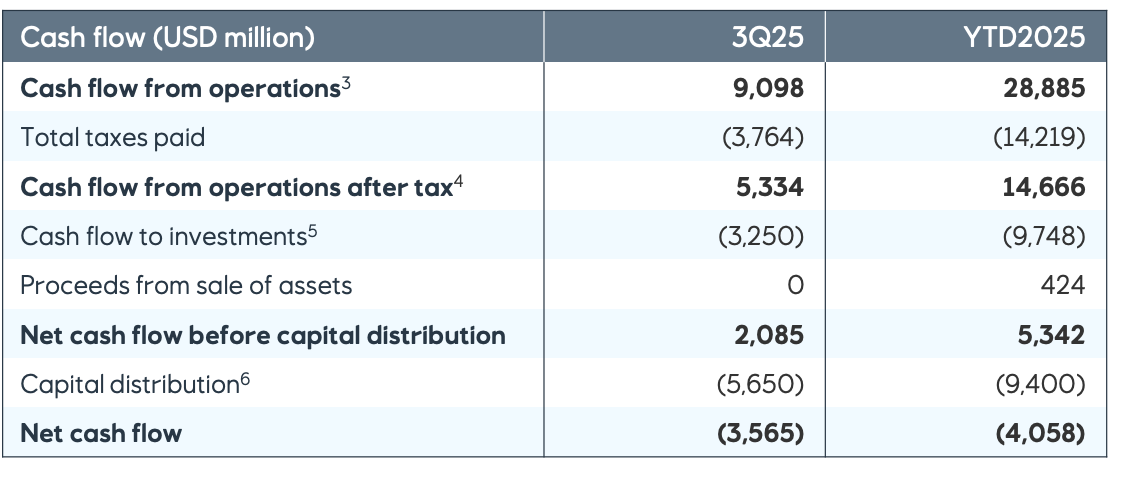

Please see the results above and CFFO is expected to increase over the next 3 years. So combining everything we rate Equinor a good company to invest. The current depressed share price should be used to add exposure to the stock. We get to collect the current 7.9% annual dividend yield.

At Muffett investments we believe that oil will have a floor of $60 and a ceiling of $80. Although many analysts are predicting sub $50 oil, we do not think that the price will be depressed for long. The middle east countries need higher oil prices to afford the generous social entitlements to their population. If they cant deliver it, we are likely to see dissent and possibly revolution and disruption of oil supply. All portfolios should have oil exposure both as a goepolitical hedge and as an inflation hedge. Equinor is one such good oil companies to consider.

We can see clear underperformance of Equinor. The market is always right and there must be some reason as to why Equinor is underperforming. We think that one of the reasons could be that its Norwegian oil production is relatively higher cost and so margins could be compressed in an environment of low oil prices. But if you believe in the hypothesis that oil will be supported at $60, then Equinor is a good stock to consider mainly for its natural gas assets.

At Muffett investments, we will be looking to add Equinor to our model portfolio starting with a smaller position and then adding to it if the price rises.

Discalimer: Analysis done in good faith and not investment advice. This is for educational purposes only. Please do own research.