Biotech series- Arrowhead pharmaceuticals:

At Muffett investments we are very interested in the developments and advances in AI. When Muffett was watching one of the podcast and one of the commentators said that the significant investments made by the hyperscalers would reduce the cost basis for the users and would be more advantageous to the users of AI rather than the hyperscalers. The market overall has a very positive view on the AI hyperscalers and they have marked the prices of these companies to very high levels.

But on the background, one of the biggest users and the beneficiaries of AI in the future would be the Biotech sector. AI can be used to integrate the knowledge gained by gene sequencing and protein folding and advances in molecular biology to target previously ‘undruggable’ areas and diseases. And currently the market is only now recognising this. We think that early entrants into this sector would be rewarded with significant gains in share prices.

Now most people will recognise CRISPR therapeutics and it has been closely associated with biotechnology. But a more important and easily targetable area is RNA therapeutics. There are several different RNA therapeutic approaches but the one we are focussing today is RNA silencing. Two important companies are involved in this. The first one is Alnylam pharmaceuticals. Today however we are going to look at another exciting RNA company called Arrowhead pharmaceuticals.

On 25//11/2025, Arrowhead pharmaceuticals reported FDA approval of one of their drug called REDEMPLO(Plozasiran), a small interfering (SiRNA) medicine as an adjunct to diet to reduce triglicerides in patients with familial chylomicronemia syndrome. The share price has since shot up to $57.71. with a year to date gains of 193%. You can see it in its share price chart comparing it with the Nasdaq 100.

source- Arrowhead pharmaceuticals

Source- Arrowhead pharmaceuticals

The success of this drug approval underpins the validity of Arrowhead’s Targetted RNAi molecule platform and increases the chances of success on other drugs under trials from the same platform. It enable long duration of action and is easy to design and produce at scale.

Source: Arrowhead Pharmaceuticals

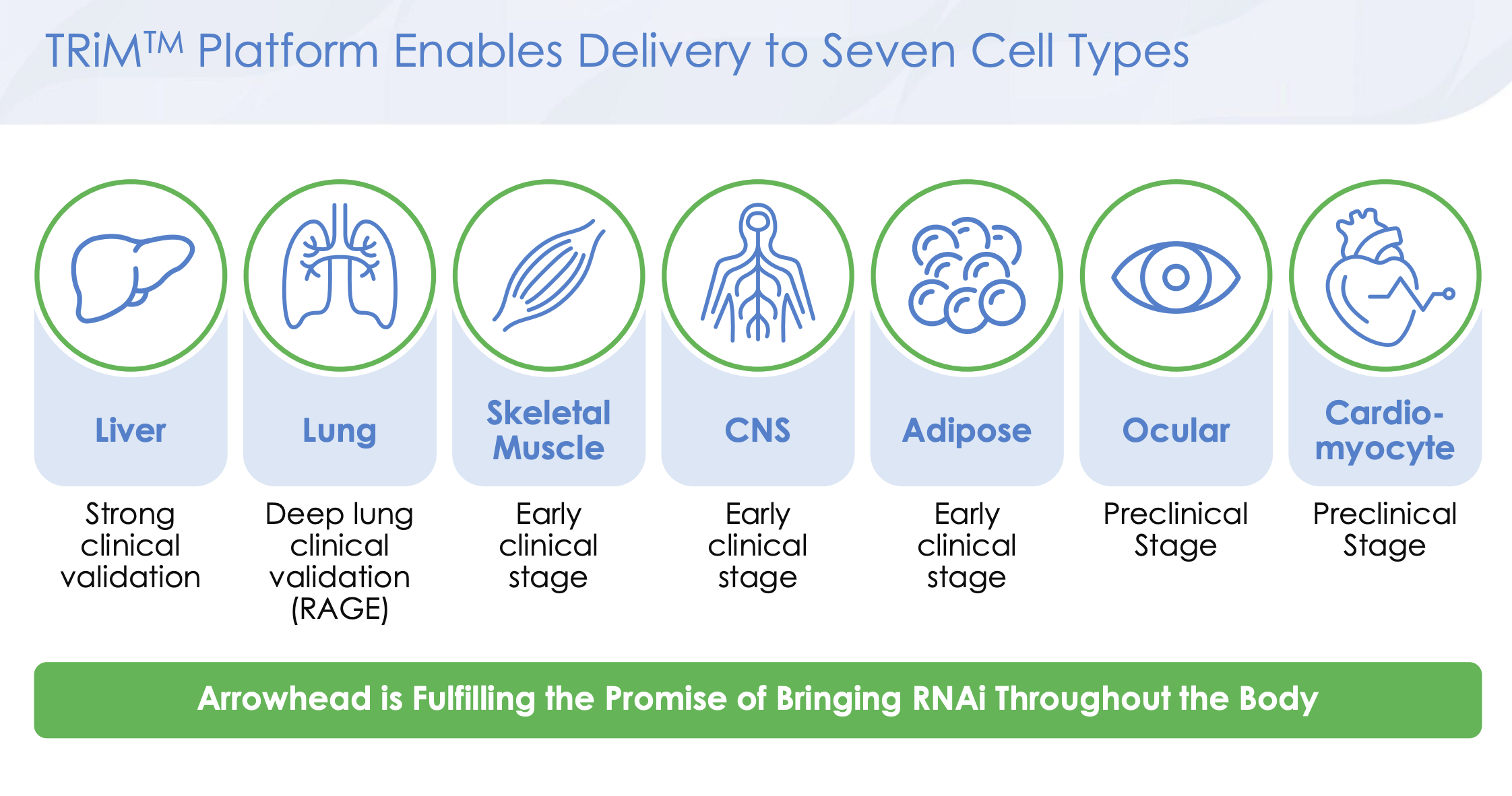

According to Arrowhead’s croporate presentation the TRiM Platform enables the delivery of drugs to seven different cell types as above. This gives a very broad therapeutic target and the ability to structure and design several drugs for different organ systems.

The above is the current pipeline of Arrowhead pharmaceuticals. We are particularly interested in the cardiometabolic and Neuromuscular areas as the TAM for this is large. There is a phase 3 trial in collaboration with AMGEN which is ongoing and this will be a game changer if the outcomes are positive as it targets Adult cardiovascular disease.

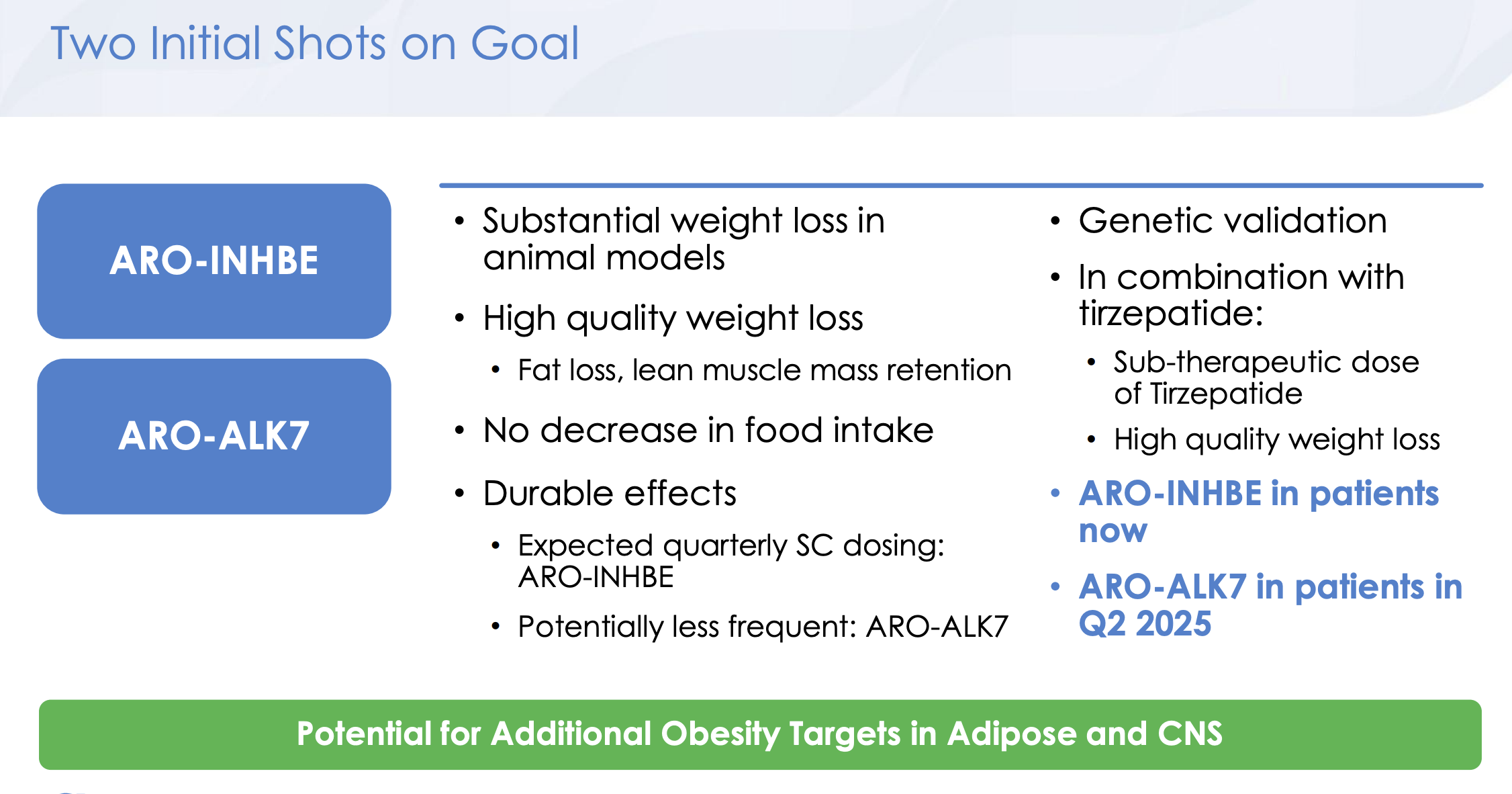

If you look closer, we have drug trials ongoing for Metabolic dysfunction associated Steatohepatitis (MASH) and there are trials with combination of Tirzapatide(Mounjaro) with Arrowhead’s drugs for obesity. This in our view will transform revenues significantly. Think of how the price of Novo Nordisk and Eli Lilly went up after their weightloss drugs.

The company has also developed a way of delivering CNS drugs with subcutaneous injection. This enables them to develop drugs for neurodegenerative disease like Alzheimers and Parkinson which have a huge TAM. See the slide below on this.

Source- Arrowhead pharmaceuticals

Many of their clinical trials are scheduled to be reported in 2026 and 2027. It is important to realise that sometimes we can have negative clinical trial data- meaning the therapeutic drug was not effective. This could tank the share price. The share price is already priced to a premium based on the recent approval of Plozasiran.

We think that Arrowhead pharmaceuticals will deliver huge returns but this is like a lottery ticket. For this reason, we should only invest in this stock with a very small percentage of the portfolio < 1%. We enter 1/2 the position size on a pullback to $50 and add to position if price goes to around $40. It is important to realise that meaningful appreciation on the stock can only happen with positive outcomes and if you are risk intolerant, then investing in Amgen ( olpasiran) or Novartis ( collaboration with Alynlam and Arrowhead) would be a better idea. But if the cardiometabolic drugs are successful at a minimum we can expect triple digit returns.

Drivers of future valuation

Commercial uptake of REDEMPLO – Early sales may be modest because of the ultra‑rare FCS population. However, if plozasiran demonstrates superiority in SHTG and dyslipidemia and wins broader approval in 2027, annual revenue could increase significantly.

Pivotal trial outcomes – Positive results from SHASTA‑3/4, MUIR‑3, OCEAN(a), and YOSEMITE are critical. Success would validate RNAi as a modality for cardiometabolic disease and could trigger milestone payments from partners.

Cash runway – With ~$782 million in cash and investmentsir.arrowheadpharma.com and milestone inflows, Arrowhead projects funding operations into fiscal 2028fool.com. This reduces financing risk.

Platform expansion – Early‑stage CNS (ARO‑MAPT and ARO‑SNCA) and neuromuscular (ARO‑DM1) programmes could open new franchises but carry high technical risk. Partnerships (e.g., Novartis) mitigate cost.

Competitive landscape – In cardiometabolic diseases, competition includes antisense (Ionis Pharma) and small‑molecule drugs. Pricing and reimbursement will influence market penetration.

At Muffett investments, we are convinced on the RNA therapeutic revolution and we think both Alynylam and Arrowhead as a buy. But we caution investors that these are risky bets and should constitute less than 1% exposure on portfolio. If the trials prove that the drugs are not effective, then we exit the position.

Disclaimer: Analysis done in good faith and not investment advice. The post is for educational purposes only and we advice the readers to seek investment advice from a qualified investment professional.