Lululemon- Attractively valued with stock trading below 2020 levels- Muffett investments

27/04/2026

Lululemon (NASDAQ: LULU) is a premium athletic apparel brand that has compounded its revenue nearly 3x in just five years — from ~$4.4B in FY2020 to over $11.1B in FY2026 (TTM). That's a track record most retailers would kill for.

But the stock has had a rough couple of years. Shares are down significantly from their 2023 highs as US growth has slowed, margins have come under pressure from tariffs and markdowns, and the company lost its long-serving CEO Calvin McDonald at the start of 2026.

We think that nervousness is creating an opportunity. Lululemon is currently trading at a PE ratio of 10.6 and has no long term debt and is growing rapidly in China with plans to expand in India through a partnership with TATA.

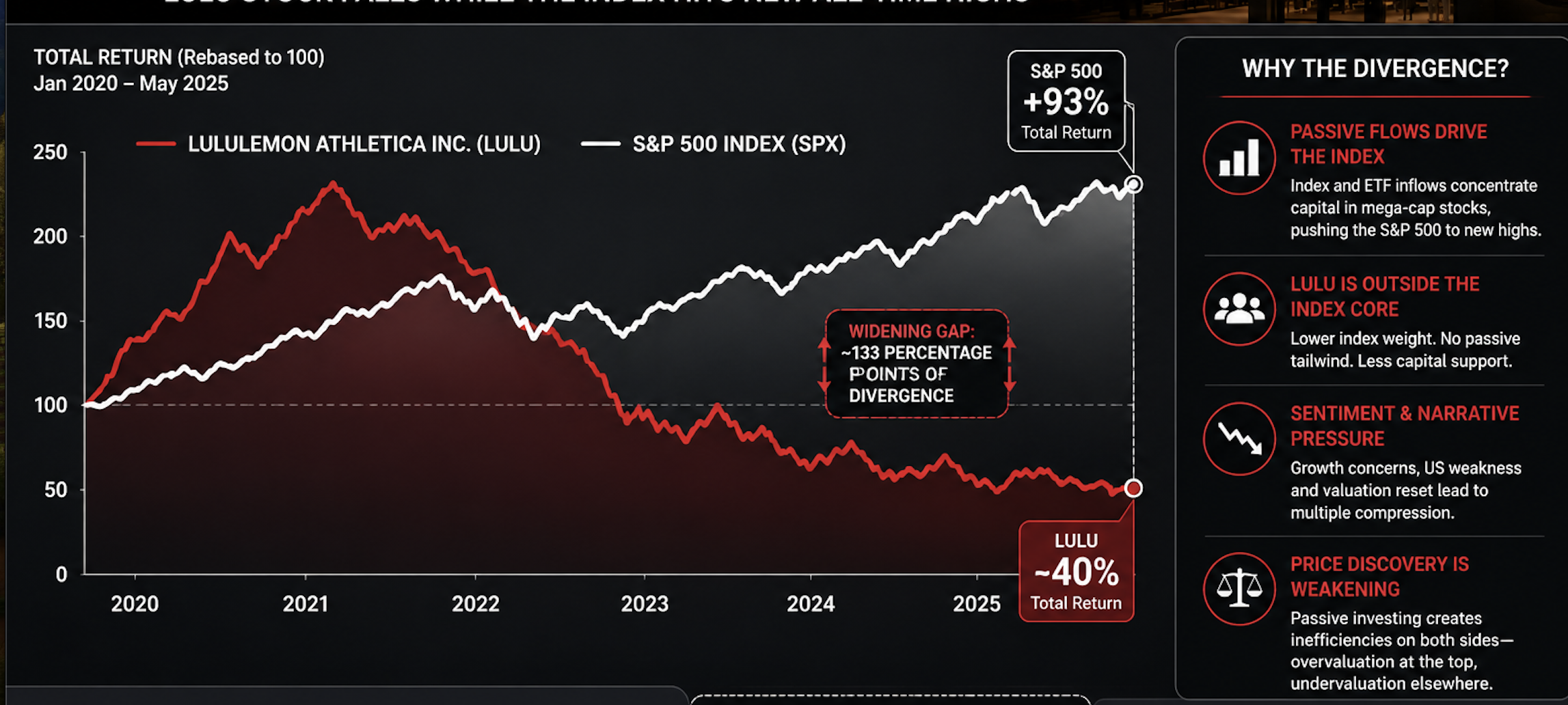

As you can see from the Chart, Lulu is now below the lows of 2020 but as pointed out the revenue is 3 times higher. This again is one of the quirks of passive investing dominance we can exploit provided we have done our due diligence.

Revenue by Region — The Story Underneath the Numbers

Lululemon's Q4 FY2025 results (reported March 2026) told a tale of two worlds:

Americas (74% of revenue): Net revenue decreased 4% YoY. Excluding the 53rd week effect from 2024, Americas was essentially flat. The US specifically fell 6%. This is the headline risk that has weighed on the stock.

China Mainland (15% of revenue): Net revenue increased 24% YoY — or a staggering 32% excluding the 53rd week. Comparable sales grew 30%. China is now contributing 15% of total revenue, up from 12% a year ago.

Rest of World (12% of revenue): Up 10% YoY, or 16% excluding the 53rd week. A quiet but steady grower.

The narrative is clear: the US is maturing, and Asia is accelerating.

Fiscal Year Revenue YoY Growth FY2020 $4.4B +11% FY2021 $6.3B +42% FY2022 $6.3B → $8.1B +29% FY2023 $8.1B — FY2024 $9.6B +19% FY2025 $10.6B +10% FY2026 (TTM) $11.1B +5%

Growth is decelerating — no question. But for a brand at $11B+ in revenue, high-single to low-double digit top-line growth backed by explosive international expansion is still a compelling story. Their "Power of Three ×2" strategy targets $12.5B by 2026 — they're on track, albeit tightly.

Financial Profile

Q4 FY2025 Snapshot:

Total Net Revenue: $3.6B

Gross Margin: 54.9% (down 550bps YoY — tariffs and markdowns the culprit)

Operating Margin: 22.3% (down from 28.9% in Q4 2024)

Net Income: $586.9M ($5.01 diluted EPS vs $6.14 a year ago)

Cash & Equivalents: $1.8B — a fortress balance sheet

Share Buybacks: Repurchased 1.4M shares for $269M in Q4 alone

The margin compression is the primary bear case. Tariffs on China-sourced goods and increased markdowns hit product margins hard — a 560bps headwind in Q4. Management is working through it with pricing adjustments and supply chain efficiency, but this will take time to normalise.

China: The Real Growth Engine

This is where the thesis gets exciting.

Lululemon hit $1 billion in China revenue in 2023 — a milestone that took many global brands a decade longer to reach. Full-year China revenue grew 29% in FY2025, and the company is projecting ~20% growth in FY2026. The brand now has 170+ stores across 41 cities, with a target of 200 stores and ambitions to make China its second-largest market globally by 2026.

What's driving this? A rapidly expanding urban middle class with a genuine appetite for health, wellness, and premium lifestyle brands. Lululemon has leaned in hard with a "hyper-local" strategy — designing products specifically for Chinese body shapes and preferences, partnering with Douyin and WeChat for digital engagement, and sponsoring high-profile cultural moments like the Formula 1 Shanghai Grand Prix (featuring brand ambassador Lewis Hamilton).

Brand awareness in China is still only in the mid-to-high teens (vs. the 30s in the US) — meaning there is a vast runway of awareness-led growth still ahead, even before market penetration deepens.

India: The Next Frontier

Here's the part that most investors aren't pricing in yet.

In H2 2026, Lululemon is entering India for the first time — partnering with Tata CLiQ (part of the Tata Group, one of India's most prestigious conglomerates) as its franchise partner. This includes a first physical store and a dedicated e-commerce presence on Tata CLiQ Luxury and Tata CLiQ Fashion.

Why does this matter?

India is now the world's most populous country, with a young, rapidly urbanising population and a booming wellness culture. Premium athleisure is still dramatically underpenetrated compared to markets like the US or even China five years ago. The Tata partnership is the right entry point — Tata CLiQ Luxury already serves India's affluent consumer base and understands the premium positioning that Lululemon requires.

This is not a near-term revenue needle-mover — India will likely be a rounding error for LULU financially in 2026. But the optionality is enormous. If Lululemon can replicate even a fraction of its China playbook in India over the next decade, the upside is extraordinary.

The Bull vs Bear case

🐂 Bull Case

China growing 25-30% with 170+ stores and massive awareness headroom

India entry in 2026 opens a billion-person market

$1.8B cash, active buybacks, no debt crisis

Americas weakness appears cyclical, not structural

🐻 Bear Case

Gross margin under pressure from tariffs — hard to model near-term

US comp sales declining — the core market is struggling

leadership uncertainty

Lululemon is a brand which is the midst of transformation. The US chapter is maturing; the Asian chapter is just beginning. For investors with patience, the combination of China's growth momentum and India's long-term optionality makes this one of the more interesting stories in global consumer right now.

The question isn't whether Lululemon can grow internationally. It clearly can. The question is whether the market will give it credit for that growth before the US headline numbers start looking better.

All analysis done in good faith and not investment advice. Muffett owns Lululemon in his personal portfolio and may hold or sell it depending on price action.

May the Peace of the Lord be with you always.